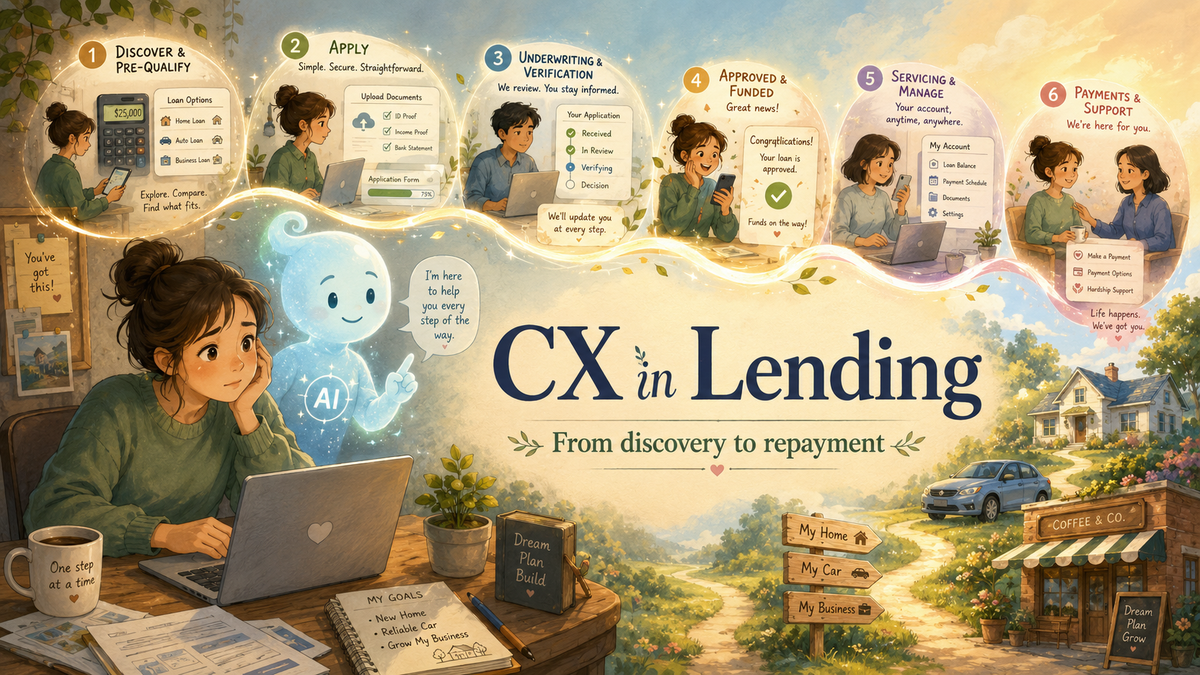

CX in Lending: The Complete Map of Use Cases and Workflows

A complete map of customer experience use cases and workflows across the lending lifecycle, from pre-application to collections and retention, and what you can actually do about each.

In lending, customer experience isn't a nice-to-have layered on top of the product. It's a big part of the product itself. Borrowers usually show up stressed and at a high-stakes moment: buying a home, covering a gap, growing a business. The process is document-heavy and tightly regulated, and the money is personal. So when an application is confusing, or a week goes by in silence during underwriting, or a collections call lands the wrong way, it doesn't just dent a satisfaction score. It drives abandonment, defaults, complaints, and churn.

This guide maps the CX use cases and workflows across the lending lifecycle, from the first ad impression all the way to the final payment and the relationship after it. For each stage, you'll find the use cases that matter and what you can actually do about them, with a focus on the automated and AI-assisted workflows that make good experience possible at scale.

The short version

- CX in lending spans the whole borrower journey, not a single support ticket, and it's inseparable from compliance.

- The biggest wins usually come from three moves: cutting application abandonment, communicating proactively, and offering real self-service.

- Automation and AI (chat, voice, agent assist, document handling) are what let you deliver a good experience at scale without ballooning headcount.

- If you can't measure it (completion rate, time-to-fund, CSAT, first-contact resolution, complaints), you can't improve it.

How to think about CX in lending

Two things make lending CX different from generic customer service:

- It's a journey, not a transaction. The relationship can run from a few months for a personal loan to a few decades for a mortgage, across acquisition, decisioning, servicing, and repayment. A bad experience early on compounds over that whole lifetime.

- Every interaction is regulated. Disclosures, adverse action notices, fair-lending rules, complaint handling, and collections constraints mean CX and compliance are really the same conversation. Whatever you build has to be pleasant and defensible at the same time.

The rest of this guide follows the borrower journey. Treat it as a checklist: for each stage, which experiences matter, and which workflows deliver them.

1. Discovery and pre-application

Before anyone applies, CX is about clarity, confidence, and easing the fear of "will I even qualify?"

- Eligibility pre-checks. Let prospects see whether they're likely to qualify without a hard credit pull. What you can do: soft-pull pre-qualification and instant "you're likely approved for X" messaging that sets expectations before the full application.

- Rate and payment transparency. Anxiety spikes when pricing is hidden. What you can do: interactive rate and payment calculators, plus personalized quote pages that update in real time as inputs change.

- Product guidance. Borrowers often don't know which product fits: fixed versus variable, term length, secured versus unsecured. What you can do: a guided "which loan is right for me" recommender or a conversational assistant that explains the trade-offs in plain language.

- Always-on pre-sales answers. Questions arrive at 11pm. What you can do: an AI chat or voice assistant grounded in your product and policy docs to answer eligibility, documentation, and process questions around the clock, with a clean handoff to a human for edge cases.

- Accessibility and language. What you can do: multilingual content and WCAG-compliant flows, so the top of the funnel doesn't quietly exclude whole segments.

2. Application and onboarding

This is where most abandonment happens. Every field, upload, and re-entry is a chance to lose the borrower.

- Friction reduction and pre-fill. What you can do: pre-fill from known data, offer bank-linking and open-banking connections, and use progressive disclosure so applicants only see what's relevant to them.

- Save and resume. Applications get interrupted. What you can do: keep progress persistent and send a proactive "you're two steps from done" nudge by email or SMS.

- Document collection. This is the single biggest source of friction. What you can do: guided upload with instant OCR validation, so if someone uploads the wrong page you catch it in seconds instead of rejecting them days later.

- Real-time status. What you can do: a live application tracker (submitted, verifying, decision) so nobody wonders whether things are stuck.

- Abandonment recovery. What you can do: triggered win-back journeys that detect drop-off and re-engage the borrower with the specific blocker addressed, whether that's a missing document or cold feet on the rate.

- Identity and fraud checks that don't feel hostile. What you can do: streamlined KYC and verification that explains why each step exists, which takes the edge off the "why are you interrogating me" feeling.

3. Verification, underwriting, and decisioning

This is the "black box" stage. Even a fast decision feels slow when it happens in silence, so the goal here is transparency and quick communication.

- Proactive status updates. What you can do: automated milestone notifications, so borrowers hear from you before they have to ask. This alone cuts a lot of "what's happening?" inbound contacts.

- Fast, clear document follow-ups. What you can do: automatically detect missing or expired documents and request exactly what's needed, with examples, instead of a vague "please provide additional documentation."

- Conditional approvals in plain language. What you can do: turn underwriting conditions into a simple checklist the borrower can actually act on.

- Adverse action, done humanely and compliantly. A decline is the highest-stakes CX moment there is. What you can do: generate compliant adverse action notices with clear reasons, and add constructive next steps so a dead end becomes a path forward.

- Agent assist for underwriters and reps. What you can do: surface the full applicant context and suggested responses to your team, so human answers stay fast, accurate, and consistent.

4. Approval, offer, and closing

The borrower said yes in principle. Now don't lose them to a clunky finish.

- Clear, comparable offers. What you can do: present terms with transparent breakdowns (APR, fees, total cost) and, where it helps, side-by-side options so the choice feels informed rather than pressured.

- Digital acceptance and e-sign. What you can do: frictionless e-signature and disclosure delivery, with confirmation that the borrower actually understood the key terms.

- Closing coordination. This matters most in mortgage, auto, and SMB lending. What you can do: orchestrate checklists and reminders across the borrower, your internal teams, and third parties like title, dealer, or broker, so nothing stalls at the finish line.

- Funding confirmation. What you can do: give an unambiguous "your funds are on the way" or "your loan is active" moment with clear next steps, which takes away a lot of post-approval anxiety.

5. Servicing and account management

This is the longest phase of the relationship, and it's where loyalty (or resentment) gets built one small interaction at a time.

- Self-service for common tasks. What you can do: let borrowers view balances, payoff quotes, statements, and due dates, and update payment methods or autopay without calling in.

- 24/7 conversational support. What you can do: use AI chat and voice assistants to resolve routine questions instantly (payoff amount, next due date, how interest is calculated) and escalate the rest with full context attached.

- Proactive account nudges. What you can do: send upcoming-payment reminders, rate-change notices, and end-of-term prompts on whichever channel the borrower prefers.

- Life-event handling. Address changes, name changes, disputes, tax statements. What you can do: build guided flows that complete these without a phone tree.

- Servicing transfers. What you can do: if a loan is sold or migrated, over-communicate the change so trust survives the handoff.

6. Payments, hardship, and collections

This is the most sensitive stage of all. Handled badly, it destroys trust and invites complaints and regulatory scrutiny. Handled well, it protects both the borrower and the portfolio.

- Frictionless payments. What you can do: offer multiple payment methods, autopay, and one-tap "pay now" straight from a reminder. A lot of missed payments are logistical, not financial.

- Early, empathetic outreach. What you can do: send pre-delinquency nudges before a payment is even missed, framed as help ("need to move your due date?") rather than a threat.

- Self-serve hardship and restructuring. What you can do: let borrowers request deferrals, payment plans, or due-date changes through a digital flow, with instant eligibility feedback instead of a dreaded phone call.

- Compliant, respectful collections. What you can do: build workflows that honor contact-time, frequency, and channel rules automatically, log every interaction, and keep the tone consistent and non-coercive.

- Sentiment-aware escalation. What you can do: detect distress, confusion, or vulnerability signals and route those conversations to trained humans quickly.

7. Retention, loyalty, and growth

Acquiring a borrower is expensive. The real return comes from the relationship that follows, so CX here is about staying relevant and rewarding loyalty.

- Proactive refinance and better-offer alerts. What you can do: watch for eligibility changes and reach out when a borrower could benefit, ideally before a competitor does.

- Contextual cross-sell. What you can do: recommend the right next product based on lifecycle and behavior (a line of credit at loan payoff, say), not a blanket promotion.

- Milestone recognition. What you can do: celebrate payoff, on-time streaks, and anniversaries. Small moments like these build advocacy.

- Referral and review capture. What you can do: ask for referrals and reviews right after a high-satisfaction moment like funding or payoff, when goodwill is at its peak.

- Win-back. What you can do: re-engage paid-off or lapsed borrowers with relevant new offers instead of letting the relationship go cold.

8. Support and complaint handling

Support runs through every stage, not just one. And in lending, complaint handling is also a regulated, board-level concern.

- Omnichannel continuity. What you can do: let a conversation move from chat to email to phone without the borrower repeating themselves, by sharing context across channels.

- Intelligent routing and triage. What you can do: classify and prioritize inquiries (billing, hardship, dispute, complaint) and route them to the right queue automatically.

- Complaint capture and tracking. What you can do: detect and log complaints reliably, track resolution against SLAs, and surface recurring themes so you can fix the root cause.

- Knowledge that stays current. What you can do: keep a single source of truth so borrowers and agents get the same correct answer, and updates propagate everywhere at once.

- Dispute resolution. What you can do: use structured flows for payment and credit-reporting disputes that keep the borrower informed at every step.

Cross-cutting capabilities that power all of it

The stage-by-stage use cases above rest on a handful of shared capabilities. Invest in these once and they pay off across the entire journey:

- Personalization: tailor content, offers, and communication to each borrower's product, stage, and behavior.

- Proactive communication: reach out before the borrower has to. It's the single highest-leverage CX move in lending.

- Self-service: deflect routine work to well-designed digital flows so your people can focus on the complex, emotional, or high-value moments.

- AI agent assist: give human reps context, drafts, and next-best-actions so every answer is fast and consistent.

- Voice and conversational AI: handle high call volumes (payoff quotes, due dates, status checks) instantly, around the clock, with human escalation when needed.

- Compliance by design: bake disclosures, contact rules, and audit logging into the workflows, so a good experience is also a defensible one.

How to measure it

If you can't measure the experience, you can't improve it. These are the metrics that matter most in lending CX:

- Application completion and abandonment rate: the clearest early signal of onboarding friction.

- Time-to-decision and time-to-fund: in lending, speed is experience.

- CSAT, NPS, and Customer Effort Score: measured at key moments, not just once a year.

- First-contact resolution and self-service containment: how much you resolve without a human escalation.

- Complaint volume and resolution time: a CX metric and a compliance metric at once.

- Retention, refinance capture, and repeat-borrow rate: the long-term payoff of good experience.

Where to start

You don't have to build all of this at once. In most lending books, the highest-return starting points are cutting application abandonment (pre-fill, guided document upload, save and resume), communicating proactively during underwriting and servicing, and offering self-service plus 24/7 conversational support for routine questions. Those three lower cost and raise satisfaction at the same time, and they set you up for the more advanced, AI-driven workflows across the rest of the journey.

The lenders who pull ahead over the next few years won't just be the ones who price risk well. They'll be the ones who make borrowing feel clear, fast, and genuinely human at every step, and who lean on automation and AI to do that at scale.

Frequently asked questions

What is customer experience (CX) in lending?

CX in lending is the sum of every interaction a borrower has with a lender across the full loan lifecycle: discovering and comparing products, applying, getting a decision, closing, making payments, getting support, and eventually paying off or renewing. Because those interactions stretch over months or years and are heavily regulated, CX in lending is as much about clarity, speed, and trust as it is about friendliness.

Why does CX matter so much in lending?

Borrowing is high-stakes and emotional, and the process is long and paperwork-heavy. A confusing application or a silent underwriting period pushes people to abandon or switch lenders, while poor collections handling can trigger complaints and regulatory risk. Good CX directly affects conversion, retention, default rates, and compliance, so it shows up on the P&L, not just in a survey.

What are the main CX use cases in lending?

They follow the borrower journey: pre-qualification and rate transparency before applying, friction-free applications with guided document upload, proactive status updates during underwriting, clear offers and digital closing, self-service and 24/7 support during servicing, empathetic and compliant handling of payments and collections, and proactive retention, refinance, and cross-sell offers afterward.

How can lenders reduce loan application abandonment?

The most effective moves are pre-filling known data, connecting bank data to avoid manual entry, breaking the form into short guided steps, validating document uploads instantly so applicants fix problems on the spot, and letting people save and resume. Triggered reminders that name the exact blocker, such as a missing document, recover a meaningful share of drop-offs.

How does AI improve customer experience in lending?

AI takes on the repetitive, high-volume work that used to create delays: answering routine questions over chat and voice around the clock, reading and validating documents, drafting compliant responses, flagging distress or confusion for a human, and giving agents the right context so their answers are fast and consistent. That frees human teams to focus on complex, sensitive, or high-value moments.

Which CX metrics should lenders track?

Start with application completion and abandonment rate, time-to-decision and time-to-fund, CSAT, NPS and Customer Effort Score at key moments, first-contact resolution and self-service containment, complaint volume and resolution time, and longer-term retention and refinance capture. Together they cover speed, effort, satisfaction, compliance, and lifetime value.